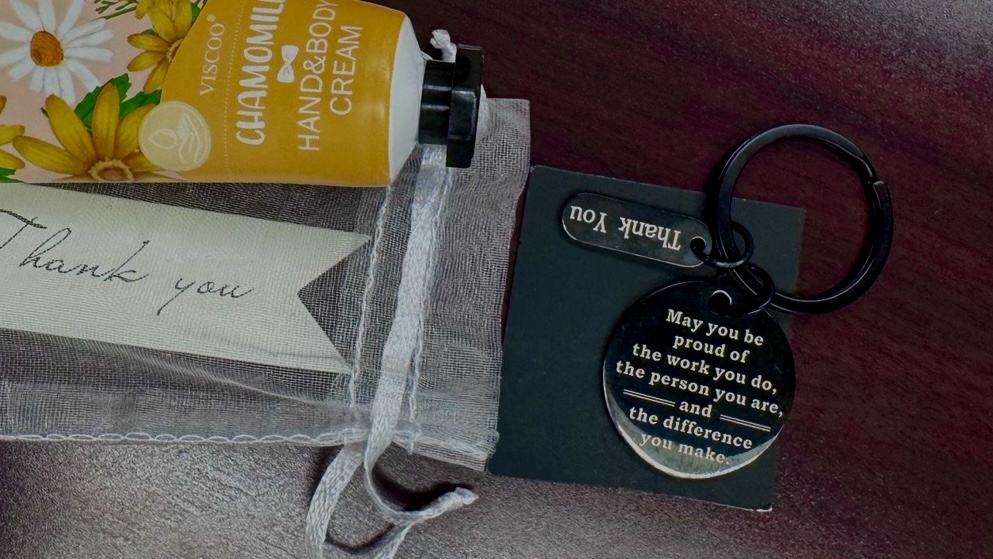

A customer at the bank gave me a gift bag last year.

The whole thing was wrapped in a white organza bag and tied with a ribbon. I want you to notice what’s in that bag, because the bag is the story. Mrs. Patterson, late 80s, Black, born into a country that spent most of her life telling her she didn’t belong in rooms like the one she now walks into to ask about her accounts, did not just grab this on her way out. She intentionally went somewhere. She picked things out. She wrote the card by hand. She tied the ribbon.

For a 15-minute conversation.

I want to tell you what I actually did to earn that bag, because the honest answer is uncomfortable: I simply had a conversation - thats all.

A few weeks earlier, I’d been reading about Trusts. Mrs. Patterson stopped by on her way out and asked what I was looking at. I told her. She mentioned, almost apologetically, that she’d been trying to figure out estate planning for a while but didn’t know where to start, didn’t know who to ask, didn’t want to look foolish in front of the wrong person. We talked for maybe fifteen minutes. I gave her the words that i was learning and found relevant - revocable, beneficiary, successor trustee... and then pointed her toward the right kind of professional to actually do the work. That was it. That was the whole intervention. She came back weeks later with the gift bag.

I work in UX research. My whole job is to identify gaps between what customers need and what institutions deliver. We map journeys. We run interviews. We build personas. We write reports that say things like “users in this segment lack confidence engaging with complex financial products.”

And then Mrs. Patterson, who lives in that exact research finding, walks up, and what she actually needs is fifteen minutes of plain English from someone who doesn’t make her feel small for asking.

Not an app. Not a chatbot. Not a redesigned disclosure document. Vocabulary. Permission. A door pointed to.

When the industry talks about financial literacy, it almost always frames the problem as something missing inside the customer - knowledge they don’t have, habits they haven’t built, behaviors that need nudging. The implied solution is always to put more information in front of them. More disclosures. More education modules. More cheerful infographics about compound interest.

But Mrs. Patterson wasn’t missing information. She had a notebook. She had bank statements. She had questions. What she was missing was a low-stakes entry point - somewhere she could ask a question without being upsold, talked down to, or routed to a 47-page PDF. The literacy gap wasn’t in her. It was in the system’s refusal to design for the conversation that has to happen before the transaction.

If you’re building for customers like Mrs. Patterson, here’s what I’ve learned matters more than any feature:

- Vocabulary is a deliverable. Most “I don’t know where to start” problems are actually “I don’t have the words to Google this” problems. The first product is often a glossary, not a flow. Designing the right entry vocabulary, the five terms someone needs to feel oriented, does more work than a polished UI.

- The fifteen-minute conversation is a feature, not an inefficiency. Banks love to talk about deflecting customers from the branch to digital channels because branches are expensive. But for a customer like Mrs. Patterson, the branch is the product. Strip out the human handoff and you’ve just designed a system that excludes her. The question isn’t “how do we get her out of the branch”, it’s “how do we make sure the branch employee she meets has the words and the patience she needs.”

- Designing for dignity beats designing for completion. Most banking products optimize for task completion: did the user finish the form, open the account, fund the transfer. Mrs. Patterson’s success metric was different. She didn’t need to complete anything that day. She needed to leave the interaction feeling like a competent adult who knew her next step. That’s a design outcome too. We just don’t measure it.

- The customers most likely to be excluded are the most loyal when included. Mrs. Patterson made - actually, she curated a gift. Card. Keychain. Hand cream. Organza bag. Ribbon. The customers whose dignity you protect become the customers who refer their entire network. This is not a soft outcome. This is retention math.

I gave Mrs. Patterson fifteen minutes off the clock, on a lunch break, because I happened to be reading about Trusts and she happened to walk by. What I gave her is not a product. It’s not a process. It’s not something that scales. It’s not something my employer can point to in an annual report. So what does it mean that the most meaningful thing I did for a customer that quarter wasn’t part of my job description?

I think it means the job description is wrong.

I think we’re measuring the wrong things.

I think Mrs. Patterson is telling us, with a hand-tied organza bag and a tube of chamomile hand cream, exactly what the design opportunity is and most of us in this industry are too busy redesigning the login screen to notice. The hand cream sits on my desk too. I haven’t opened it. I don’t think I will.

If you’re working on financial inclusion, customer experience for underserved segments, or the design of trust itself, I’d love to talk. Get in touch.